by Kelly Hill, Director – q4 financial

There’s been a lot of chatter in the press recently about what you need for a “comfortable” retirement.

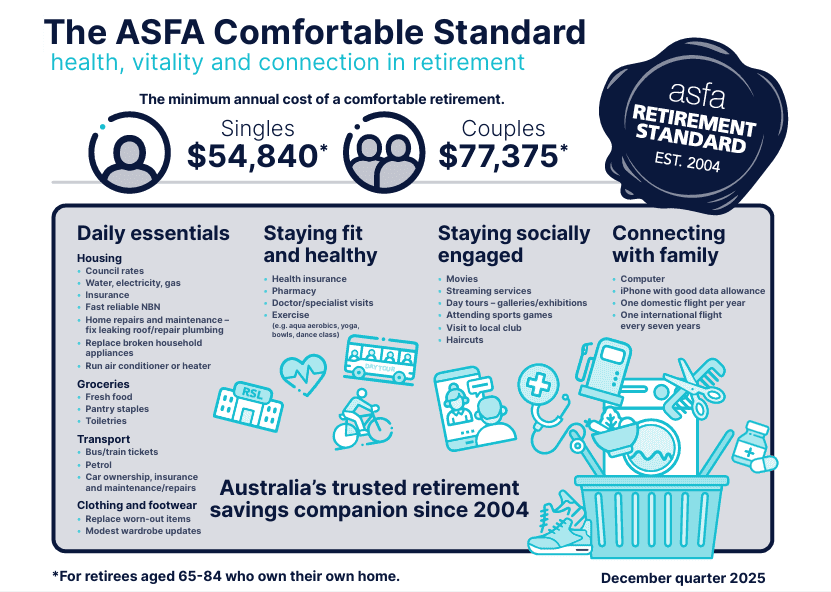

The latest update to the Association of Superannuation Funds of Australia (ASFA) Retirement Standard suggests that a couple needs around $730,000–$750,000 in superannuation (in addition to a part Age Pension) to achieve what it defines as a “comfortable” retirement.

When a doctor recently asked me for my thoughts, my response was simple:

“That’s not the kind of retirement I’m wishing for.”

And I suspect it’s not the kind most medical professionals are wishing for either.

What does “comfortable” actually mean?

The Association of Superannuation Funds of Australia Retirement Standard is based on detailed modelling. It estimates the annual spending required for two retirees and reverse-engineers the super balance required to fund it.

But here’s the key question:

Comfortable according to whom?

The ASFA assumptions typically include:

- Modest domestic holidays

- Limited overseas travel

- Replacing cars periodically (not luxury vehicles)

- Dining out occasionally

- A relatively conservative lifestyle

- A home already owned outright

- Partial reliance on the Age Pension

It is not built around:

- Extended overseas travel

- Supporting adult children

- Premium healthcare and wellbeing choices

- Helping grandchildren with education

- Ongoing philanthropy

- Funding business interests or investment opportunities

- Leaving a substantial legacy

There’s nothing wrong with the ASFA benchmark. It serves a purpose.

But it is a baseline — not an aspiration.

The cost of living reality

For the first time in three years, ASFA has increased its retirement spending numbers.

One of the main drivers?

The Age Pension is struggling to keep pace with cost-of-living pressures.

The categories retirees spend heavily on — insurance, healthcare, energy, food, travel — are rising faster than pension indexation.

This matters because the $750,000 figure assumes a level of ongoing government support.

If that support lags behind real-world costs, your capital must work harder.

The aspirational retirement

At the Brisbane Local Medical Association educational event in July 2024, I presented a deliberately bold assumption.

I asked attendees to imagine:

- You want retirement income equal to your current gross income (I deliberately used a conservative assumption of $200,000).

- You want to maintain your capital forever.

- You assume a 5% return.

- You ignore inflation (which, in reality, makes the number higher).

The capital required?

Approximately $4 million.

That’s not designed to shock. It’s designed to reframe.

Because the real question isn’t:

“What is comfortable?”

It’s:

“What do I want my life to look like?”

What a Doctor’s retirement actually looks like

In reality, the doctors we work with typically want:

- Choice about when to stop working (or slow down)

- Flexibility to travel well and often

- The ability to upgrade homes or relocate

- Financial support for children and grandchildren

- Protection from market volatility

- The capacity to say “yes” to opportunities

- A meaningful estate and legacy

That requires choice.

And choice requires capital.

$750,000 might be enough — but enough for what?

The danger of media headlines is that they anchor expectations.

If you’re earning $300,000–$600,000+ per year during your working life, and living accordingly, the step down into a “comfortable” ASFA retirement would feel unbearable.

There is nothing wrong with choosing a simpler retirement.

But it should be a deliberate decision — not an accidental one driven by undercapitalisation.

At q4 financial, we don’t sit on the fence.

We don’t plan for “just enough.”

We plan for choice.

The better question to ask

Instead of asking:

“Is $750,000 enough?”

Ask:

- What do I wish for in retirement?

- What income will this require?

- Do I want to preserve capital or draw it down?

- Do I want government reliance or independence?

- What legacy do I want to leave?

- What does freedom actually look like for me?

The number only makes sense once the vision is clear.

Start with the end in mind

Retirement is not a financial milestone.

It’s a lifestyle decision funded by capital.

If you attended the BLMA session last year, you’ll remember we spoke about starting with the end in mind — then working backwards.

The earlier you clarify your aspirational retirement, the more achievable it becomes.

If you’d like to sense-check your own number — beyond the headlines — we’re always happy to have that conversation.

Because “comfortable” is a benchmark.

But aspirational?

That’s personal.