by Kelly Hill, Director – q4 financial

There’s been a lot of commentary in the media recently about how much you need to retire.

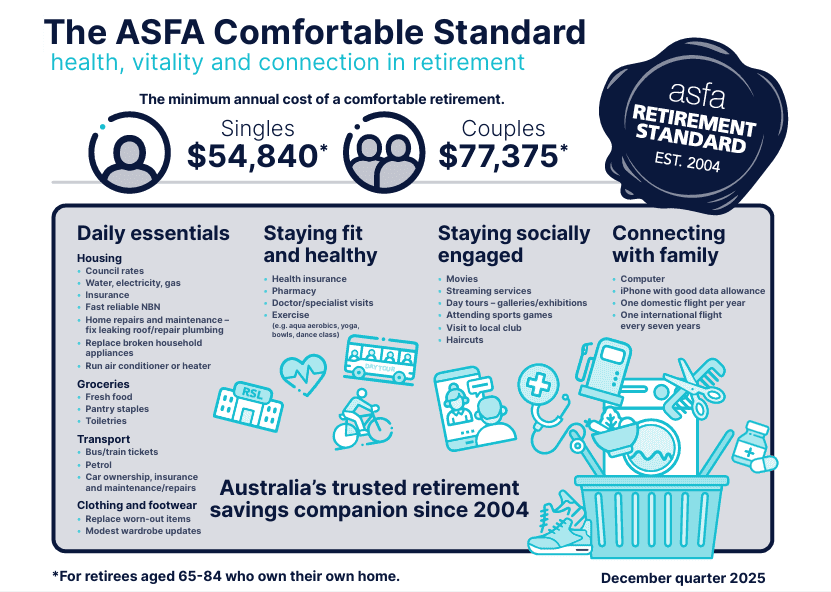

The latest update to the ASFA Retirement Standard suggests that a couple needs around $730,000–$750,000 in superannuation (alongside a part Age Pension) to achieve what is described as a “comfortable” retirement.

When people ask for my view on this number, my response is usually the same:

That’s not the kind of retirement most of our clients are planning for.

Because while the ASFA benchmark is useful, it represents a baseline lifestyle — not necessarily an aspirational one.

And for many business owners, professionals and self-funded retirees, the gap between those two can be significant.

What does “comfortable” actually mean?

The ASFA Retirement Standard is based on detailed modelling of what retirees typically spend across categories like housing, food, health care, transport, leisure and travel.

For a couple, a “comfortable” retirement currently assumes spending of roughly $70,000–$75,000 per year.

It includes things like:

- Modest domestic holidays

- Occasional overseas travel

- Dining out periodically

- Replacing cars every several years

- Maintaining private health insurance

- Living in a home that is already owned outright

There is absolutely nothing wrong with this standard.

But it’s important to recognise that it reflects an average lifestyle — not necessarily the lifestyle many professionals or business owners want after decades of hard work.

The cost-of-living reality

One of the reasons the retirement standard has recently increased is the pressure of rising costs.

Many of the categories retirees spend heavily on — healthcare, insurance, food, energy and travel — are increasing faster than government support payments.

This matters because the $750,000 figure assumes ongoing support from the Age Pension.

For Australians who want to remain largely self-funded and independent, the amount of capital required is often significantly higher.

Comfortable vs aspirational retirement

At q4 financial, we often talk about the difference between “comfortable” and “aspirational.”

A comfortable retirement might mean:

- Living within a defined annual budget

- Travelling occasionally

- Being mindful of major spending decisions

An aspirational retirement usually looks different.

For many business owners and professionals, it includes:

- The flexibility to travel regularly and well

- Upgrading homes or relocating

- Supporting children or grandchildren

- Helping with education or first home deposits

- Maintaining a high standard of health care

- Having the freedom to say yes to opportunities

- Leaving a meaningful legacy

That level of choice and flexibility requires more financial capacity.

And that capacity comes from having sufficient capital behind you.

The question isn’t “What’s enough?”

The danger with headlines like “$750k is enough to retire” is that they can anchor expectations.

But retirement planning shouldn’t start with someone else’s number.

It should start with a far more important question:

What do you want your life to look like?

Your ideal retirement might involve:

- More travel

- More time with family

- Pursuing new interests or business ventures

- Living in multiple locations

- Giving back through philanthropy or mentoring

Once that picture is clear, the financial plan becomes much easier to build.

Start with the end in mind

One concept we often discuss with clients is starting with the end in mind.

Instead of asking “How much do I need to retire?” we ask:

- What income do you want in retirement?

- Do you want to preserve capital or draw it down?

- How important is financial independence from government support?

- What legacy would you like to leave?

The answers to these questions shape the capital required.

For some people, $750,000 may be enough.

For others, it may fall well short of the lifestyle they have worked hard to build.

Planning for choice

At q4 financial, we don’t plan for “just enough.”

We plan for choice.

Choice about when you stop working.

Choice about how you spend your time.

Choice about how you support the people and causes that matter to you.

Because retirement isn’t simply about reaching a number.

It’s about creating the freedom to live the life you want.

The earlier you clarify your aspirational retirement, the more achievable it becomes.

If you’d like to sense-check your own number — beyond the headlines — we’re always happy to have that conversation.

Because “comfortable” is a benchmark.

But aspirational?

That’s personal.